The UK Shell Pension Plan

Your pension in focus

Plan now – your future matters

Issue 12

2025

Chair’s welcome

Welcome to the annual newsletter from the Trustee of the UK Shell Pension Plan (UKSPP).

As the new Trustee Chair, I would like to extend sincere thanks and appreciation to David Bunch for his dedication to the UKSPP. After three years as Chair of the UKSPP, David stepped down from the role in July 2024. He did an excellent job leading the Plan through some periods of economic and market volatility. David remains with Shell and has taken on an exciting new opportunity as EVP Mobility.

I’m pleased to have taken on this new role as Chair and am looking forward to working alongside the other Trustee Directors to ensure the continued success of the Plan, which offers some of the best employer contribution rates in the UK.

Every three years, we conduct a comprehensive review of our investment strategy to ensure it continues to meet the evolving needs of UKSPP members.

The most recent review allowed the Trustee to make informed adjustments to the UKSPP’s investment strategy, ensuring it remains robust and forward-looking.

The changes to the investment strategy affect most members, so I encourage you to look out for your personalised email from Fidelity in April 2025. This email will explain the changes and how they will affect the investment of your UKSPP pension account.

In the meantime, you can find a summary of the changes and what it means for you on pages 4 to 6.

You’ll still be able to view your investments by logging in to PlanViewer or downloading the app.

For members nearing retirement, we have news about a new retirement solution created by Fidelity. You can find details about the Fidelity Retirement Master Trust on page 7.

Finally, on page 13, you’ll find a summary of the UK Chancellor of the Exchequer’s proposal to change pension rules in relation to inheritance tax (IHT).

Parminder Kohli

Chair of the Trustee

2

Chair’s welcome continued

I hope you find your UKSPP newsletter informative and helpful as you continue your retirement savings journey.

Parminder Kohli

Chair of the Trustee

At a glance

In this edition

3

Investment strategy review

Every three years we review the UKSPP’s investment strategy to ensure it continues to meet the needs of UKSPP members, and that it reflects the Trustee’s investment beliefs. As a result of the latest review, the Trustee has decided to make changes to the Plan’s investment options, including the default investment fund.

As a UKSPP member, you can choose how your UKSPP account is invested, or you can remain in the the Plan’s default investment option – currently the ‘Drawdown Lifestyle’.

In May 2025, the Drawdown Lifestyle (together with the annuity and cash lifestyle) will be closed, and all members’ pension accounts that are currently invested in the Lifestyle arrangements will be transferred to the new default investment option – “Futurewise” (a Target Date Fund).

Why is a change being made?

FutureWise offers an innovative and streamlined approach to retirement investing, closely mirroring the current lifestyle strategy.

FutureWise is designed to optimise your pension savings by allocating higher-returning assets when you are many years away from retirement and gradually shifting to lower-risk assets as you approach your retirement date.

The key differences between the current default fund option and FutureWise are explored on the next page.

4

Simplified investment management – Under the current lifestyle strategy, fund switches are managed using a bespoke approach set by the Trustee, ensuring that your investments automatically adjust based on your selected retirement age. However, with FutureWise, all these transitions are managed within the fund itself, with target date fund five-year retirement windows.

A mix of investments – This change allows the Trustee to use Fidelity’s expertise in asset management and access a broader range of investment options. By doing so, the Trustee can reduce overall risk and potentially achieve higher growth rates for your pension savings.

Equities

Bonds

Illiquid Asset Classes e.g. real estate

45

40

37

34

31

28

25

22

19

16

13

10

7

4

1

Years to retirement

Designed with retirement in mind – Futurewise is specially designed to give you the flexibility to retire at any point in a five-year window.

We believe the target date aspect of the FutureWise Fund will provide you with more flexibility on when you might want to access your pension account.

FutureWise also currently has lower fees compared to the current lifestyle option, so more of your savings will remain invested.

We believe that for those who don’t want to choose for themselves, FutureWise will be the best option for most members.

To find out more about FutureWise, please keep an eye out for a personalised email from Fidelity, which will be arriving in early April. This email will provide you with all the details you need to know.

5

We’ve also reviewed the Plan’s self-select funds. To streamline the self-select range we’ve removed some of the funds that have been less popular or have underperformed and introduced some new ones.

The following Funds will be removed:

The following funds will be introduced:

Please be aware that the new funds are not intended to be a straight swap from one to the other. If you’re considering making any changes to your investments, we always recommend you speak to a financial adviser before making a decision.

We have written separately to members who had pension savings invested in the funds due to be removed. If you are thinking of switching any of your investments, the Nordea, M&G fund and the HSBC fund mentioned above are now available on PlanViewer.

6

Introducing the Fidelity Retirement Master Trust: A retirement solution

Retirement planning can be a daunting task, with numerous options and decisions to consider.

For many members, finding the right retirement solution can be challenging. That’s why Fidelity have created the Retirement Master Trust, a new decumulation solution designed for members who prefer a straightforward, reliable option without the need to search for alternatives.

There are many options available to you when you decide to take your pension savings:

You can’t take your money directly from your UKSPP account, so this is why you need a decumulation solution.

The Fidelity Retirement Master Trust is specifically designed to provide drawdown in retirement as well as access to other retirement options, ensuring that your hard-earned savings continue to earn investment returns throughout your retirement years.

7

Why Choose the Fidelity Retirement Master Trust?

As you near your target retirement date, Fidelity will write to you with details of all the options available to you, including the option to transfer to the Fidelity Retirement Master Trust.

If you have any questions or would like additional information in the meantime, please don’t hesitate to contact Fidelity’s support team.

While the Retirement Master Trust is an option for UKSPP members to transfer to at retirement, we still strongly recommend seeking financial advice before making any decisions regarding your UKSPP account. Professional guidance or advice can help you make informed choices that best suit your individual circumstances.

8

The chart below shows how the funds that make up the current default investment option, the ‘Drawdown Lifestyle,’ performed over the last 5 years to 31 December 2024, compared with each fund’s benchmark.

|

1 Year |

3 Year |

5 Year |

||||

|---|---|---|---|---|---|---|

|

Growth Fund |

14.5 |

14.9 |

6.2 |

6.3 |

9.5 |

9.3 |

|

Transition Fund |

9.9 |

10.5 |

4.3 |

6.6 |

3.6 |

5.4 |

|

Pre-retirement Fund |

-0.1 |

0.5 |

-5.0 |

-3.8 |

-1.2 |

-0.2 |

Actual performance

Benchmark

When markets experience volatility, you may see fluctuations in the value of your pension savings. These are a normal part of long-term investing, as the value of investments can go down as well as up.

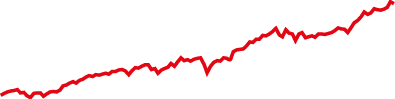

To show how investments have performed over the long term, we’ve also included performance results for the Growth Fund over the last 10 years in the graph below.

0

50

100

150

200

250

300

‘15

‘16

‘17

‘18

‘19

‘20

‘21

‘22

‘23

‘24

The chart shows the growth in fund value based on an initial investment of £100 into the UKSPP Growth Fund in January 2015, assuming no further contributions.

9

2024 was a positive year for most major equity markets. Inflation remained higher than expected. This meant that central banks were unable to cut interest rates as much as they had hoped, which led to falls in the value of many bond markets.

The UKSPP Growth and UKSPP Transition Fund, both of which are key components in the default lifestyle, delivered strong positive returns after charges. Most self-select investment fund choices delivered positive returns after charges over the year, except the Fidelity iShares Over 5 Years Index Linked Gilt Fund and Fidelity Pension Annuity Fund, which both delivered negative returns over the year after charges.

Equity investments performed the strongest over the year, and this was reflected in the performance of fund choices that have a high allocation to equities.

As a result, the following funds all delivered strong double-digit growth over the year:

Members invested in the UKSPP Transition Fund also experienced strong positive investment performance over the year. The UKSPP Pre-Retirement Fund delivered marginally negative returns over the year, and has also fallen in value over 3 and 5 years.

Jit Parekh – Investment Adviser (Aon)

Jit Parekh, CFA

Investment Adviser (Aon)

We welcome Jit Parekh, who has replaced Jo Sharples as the UKSPP’s Investment Adviser.

10

These days, lots of life’s admin can be completed online and at a time that suits you, and your UKSPP account is no exception.

Download the PlanViewer app, register your details and you can:

Registering is easy; just make sure you have your National Insurance number and your Fidelity reference to hand. Both are on your latest benefit statement.

The app uses two factor authentication when you log in, ensuring your pension plan details stay safe and secure.

11

Pensions are a tax-efficient way to save for your future. But there are limits on how much you can pay into your pension before you have to pay a tax charge. Here is some of the jargon explained.

The amount you can contribute to a UK registered pension scheme in a single tax year without incurring Annual Allowance tax charges. It is currently £60,000 but it may be lower (tapered) if your earnings exceed £200,000.

The amount you can pay into a defined contribution pension, once you’ve started to receive money from another defined contribution pension, whilst still receiving tax relief is £10,000.

The lowest amount your annual allowance can be reduced to if your income exceeds £200,000. For the current tax year, the minimum tapered annual allowance is £10,000.

If you’re concerned about exceeding the annual allowance, you can use the Fidelity Annual Allowance calculator.

If you do need to pay tax on any pension savings above the annual allowance, you can request that the Scheme does this through ‘Scheme Pays’.

Scheme Pays is the option to pay an annual allowance charge from your pension account.

There are two types of Scheme Pays and depending of the tax charge due, you may need to request one or both of them:

A request for a charge to be paid by mandatory scheme pays can be made when:

This request must be submitted to Fidelity by 31 July in the year after the tax change is due.

If an annual allowance charge is payable and is not covered by mandatory scheme pays, it may be payable by Voluntary Scheme Pays.

This request must be made by 30 November in the same year as the change is due.

12

The Lump Sum Allowance (LSA) and the Lump Sum and Death Benefit Allowance (LSDBA) are two new allowances introduced to replace the Lifetime Allowance (LTA) from 6 April 2024.

Lump Sum Allowance (LSA): This caps the total tax-free lump sum that can be paid from all your pensions when you take your retirement savings. The maximum amount is set at £268,275, which is the same as the previous LTA.

Lump Sum and Death Benefit Allowance (LSDBA): This caps the tax-free lump sum that can be paid from all your pensions when you die. The maximum amount is set at £1,073,100, which is also the same as the previous LTA.

Any lump sums taken beyond these limits will be subject to income tax at your marginal rate. If you have existing LTA protections, the limits may be higher.

If you think you might exceed, or be close to exceeding these allowances, you can find more information on the Gov.uk website.

Tax and pensions can be a complex subject – if you’re concerned about how these changes might affect you, then please speak to an independent financial adviser. You can find details of how to contact an adviser by going to www.vouchedfor.co.uk.

As part of the 2024 Autumn Budget, the Chancellor of the Exchequer announced that the Government will extend the range of pension death benefits that will become subject to inheritance tax (IHT) when someone has passed away.

If the change comes into force pension scheme administrators will be responsible for calculating and deducting any IHT owed on pension benefits.

What this means for you

There’s no change to your pension.

It’s important to note that this is currently a proposal only and is undergoing a technical consultation during 2025. If it becomes law, the new measures will come into effect on 6 April 2027.

We’ll keep you updated as the consultation progresses.

13

The 2025 UKSPP calendar

April: Investment change announcement

Look out for your letter and FAQs from Fidelity, explaining the changes to the UKSPP investments. There will also be a webinar on 30 April 2025, to explain these changes in more detail. You can register for the webinar at events.teams.microsoft.com/event

June: FutureWise

The UKSPP new default fund, FutureWise is launched.

Your annual benefit statement

Watch for the emails to view your 2025 statement in PlanViewer and the video statement.

July: Mandatory Scheme Pays

If you exceeded the standard annual allowance in the 2023/24 tax year, the deadline to request that the charge is paid by the Plan is 31 July 2025.

September: Pension Awareness week

Fidelity provides activities and resources to help you understand and value your pension

November: Voluntary Scheme Pays

If your annual allowance was tapered and you exceeded it in the 2024/25 tax year, the deadline to request that the charge is paid by the Plan is 30 November 2025.

14

Later this year, Emma Stone’s term as a Member Nominated Director (MND) will come to an end. We will be carrying out a selection process, which will be open to all eligible UKSPP members.

We’ll be in touch nearer the time with more details about the role, how the process works and how to apply.

UK Country Chair

Chair of UK Shell Pension Plan Trust Limited since July 2024.

Parminder has academic qualifications from institutions in America, Europe and India. It may therefore come as no surprise to hear that he loves to travel – he has visited almost 90 different countries so far! Away from work and travel, Parminder places great value on both physical and mental fitness and is a keen participant in yoga, meditation and running.

Alan Howard

Head of UK Pensions

Joined the Board in May 2016.

Emma Stone

Member Nominated Director (MND)

Joined the Board in October 2021.

Bhavin Kotecha

VP HR UK

Joined the Board in December 2022.

Sam Critchlow

VP Corporate Finance

Joined the Board in June 2023.

15

Fidelity’s Pension Service Centre on

0800 3 68 68 69 (UK)

or (+44) 1737 838 585 (outside the UK).

Visit Fidelity’s PlanViewer

PlanViewer is Fidelity’s online account service for UKSPP members, where you can view your current pension account or find more general pensions news and financial tips.

FIL Life Insurance Limited,

Beech Gate, Millfield Lane,

Lower Kingswood,

Tadworth, Surrey,

KT20 6RP

The Secretary to the UK Shell Pension Plan Trust Limited,

Shell Centre, London,

SE1 7NA

Or email: SI-UKSPP-Trustee@shell.com

To find impartial advice, go to:

The law gives people control over how their personal information is collected, stored, shared and used.

You can find a Privacy Notice which provides information about your personal data and how it is processed by or on behalf of the Trustee of the UKSPP on the pensions website.